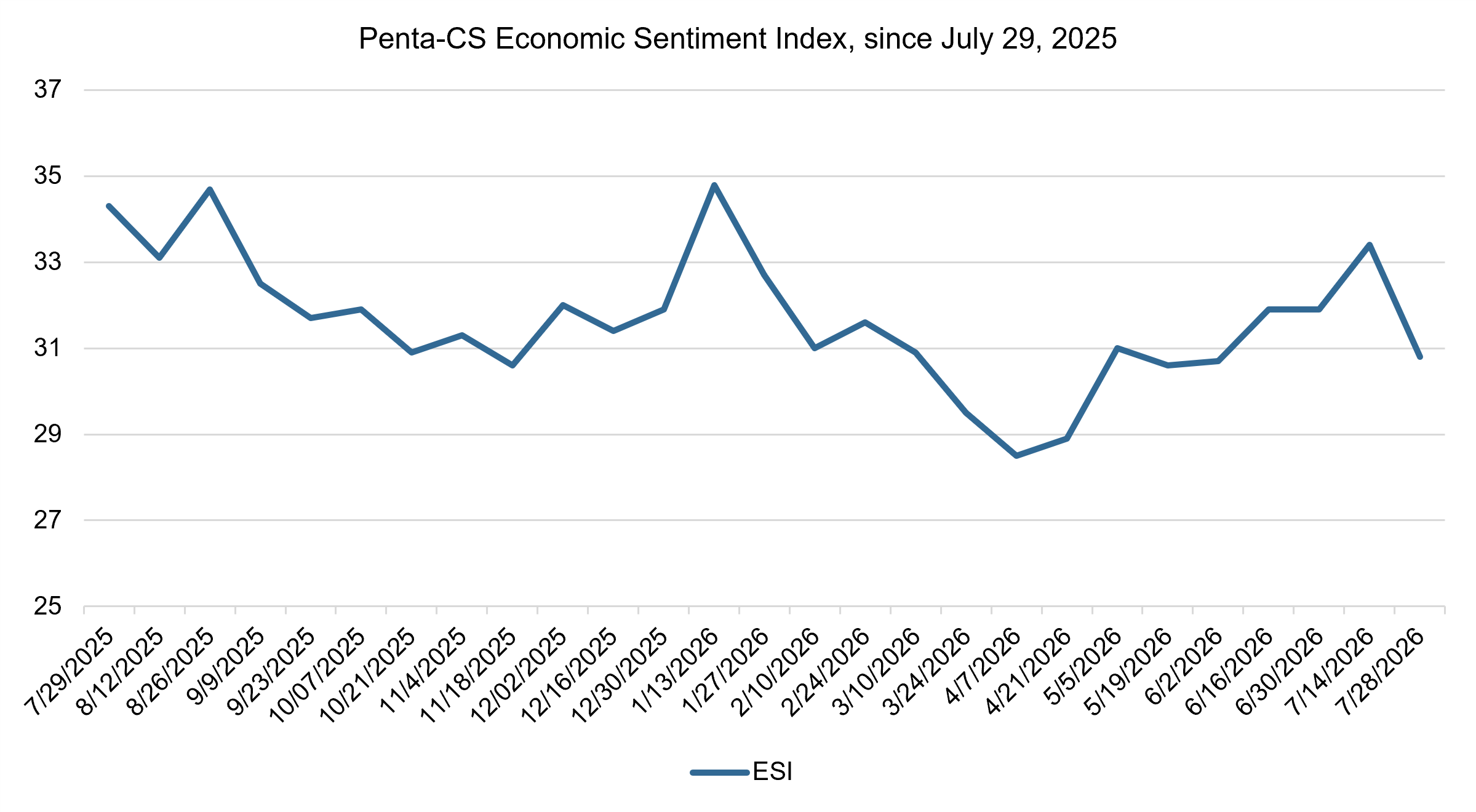

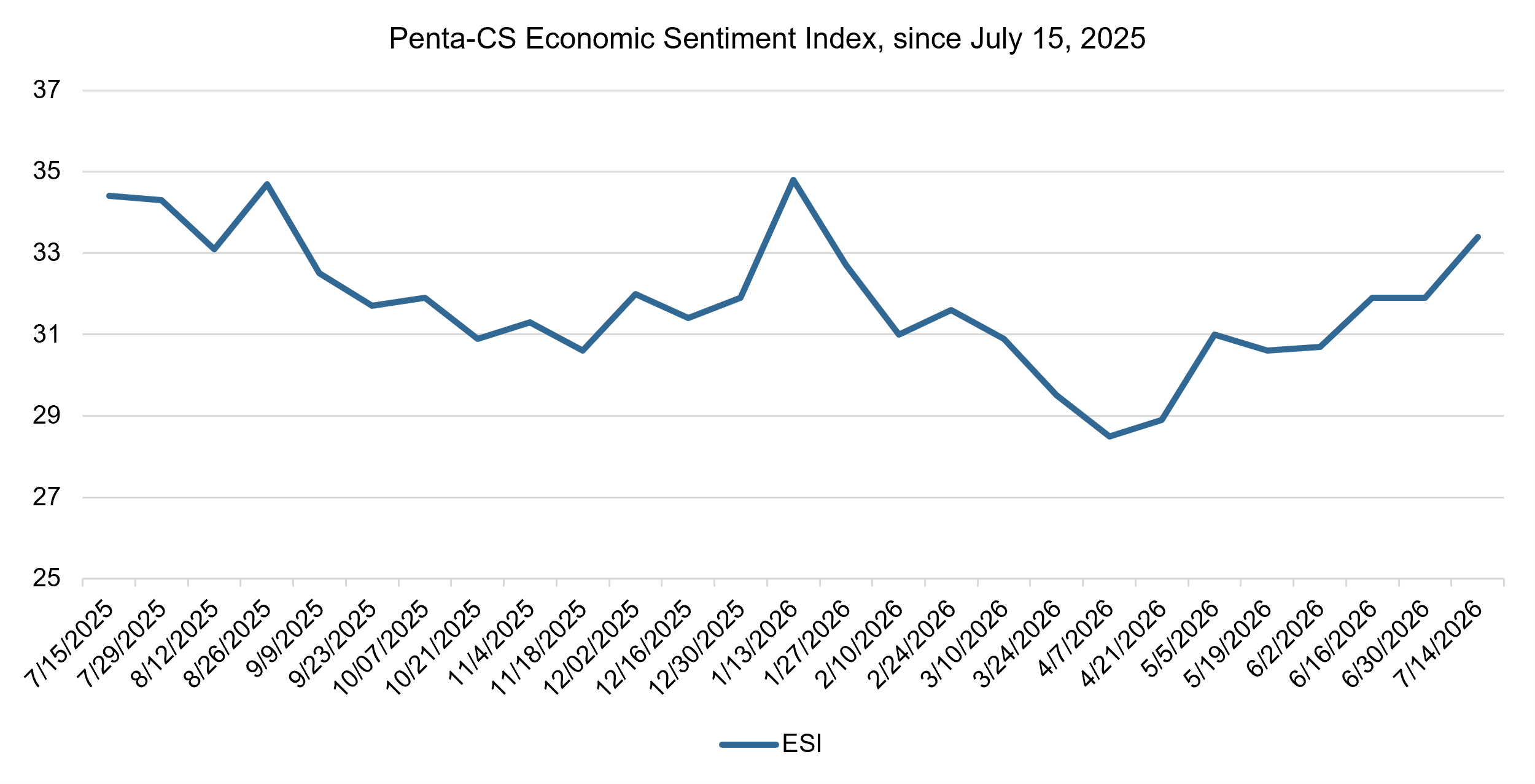

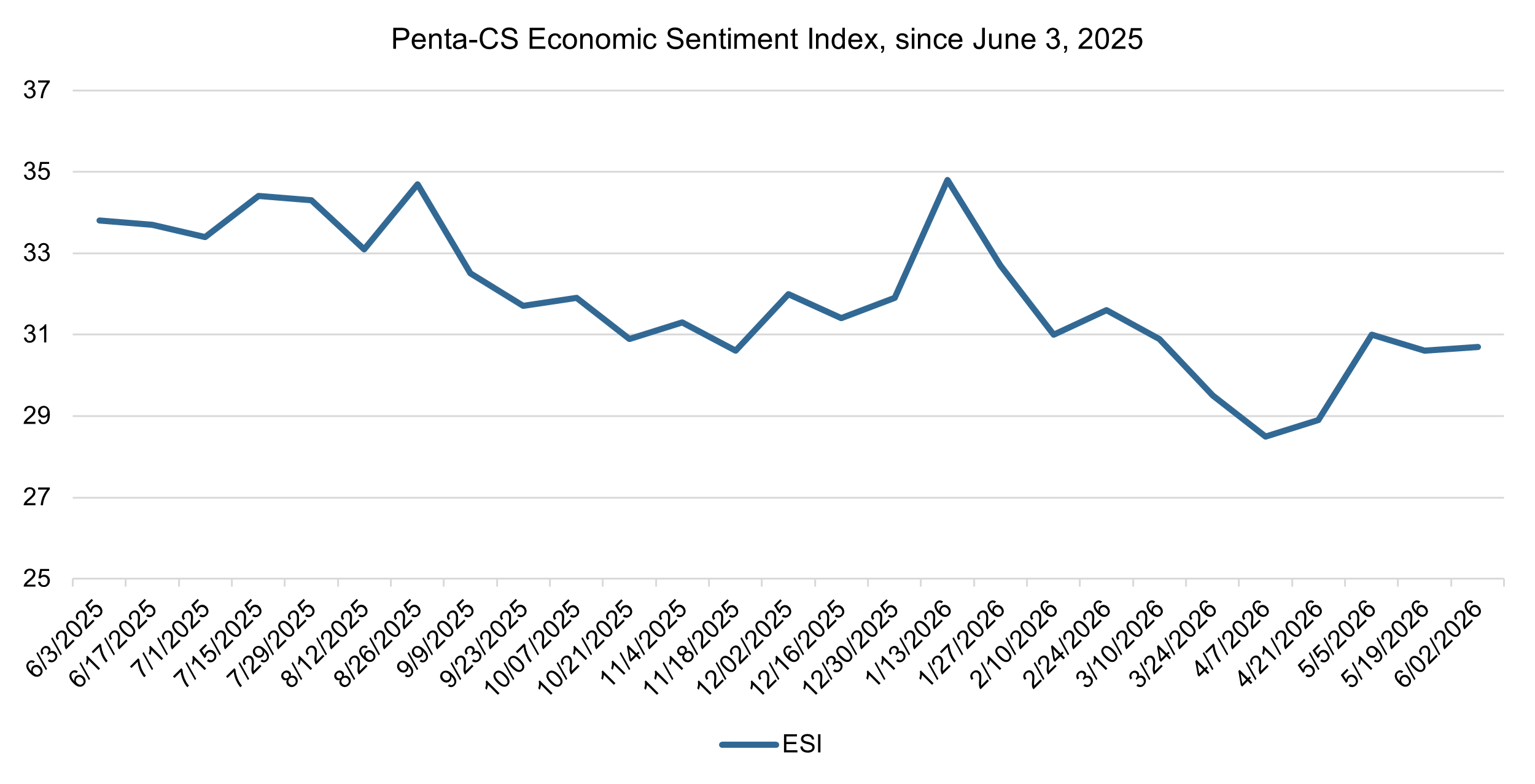

Economic sentiment declines ahead of the July FOMC meeting

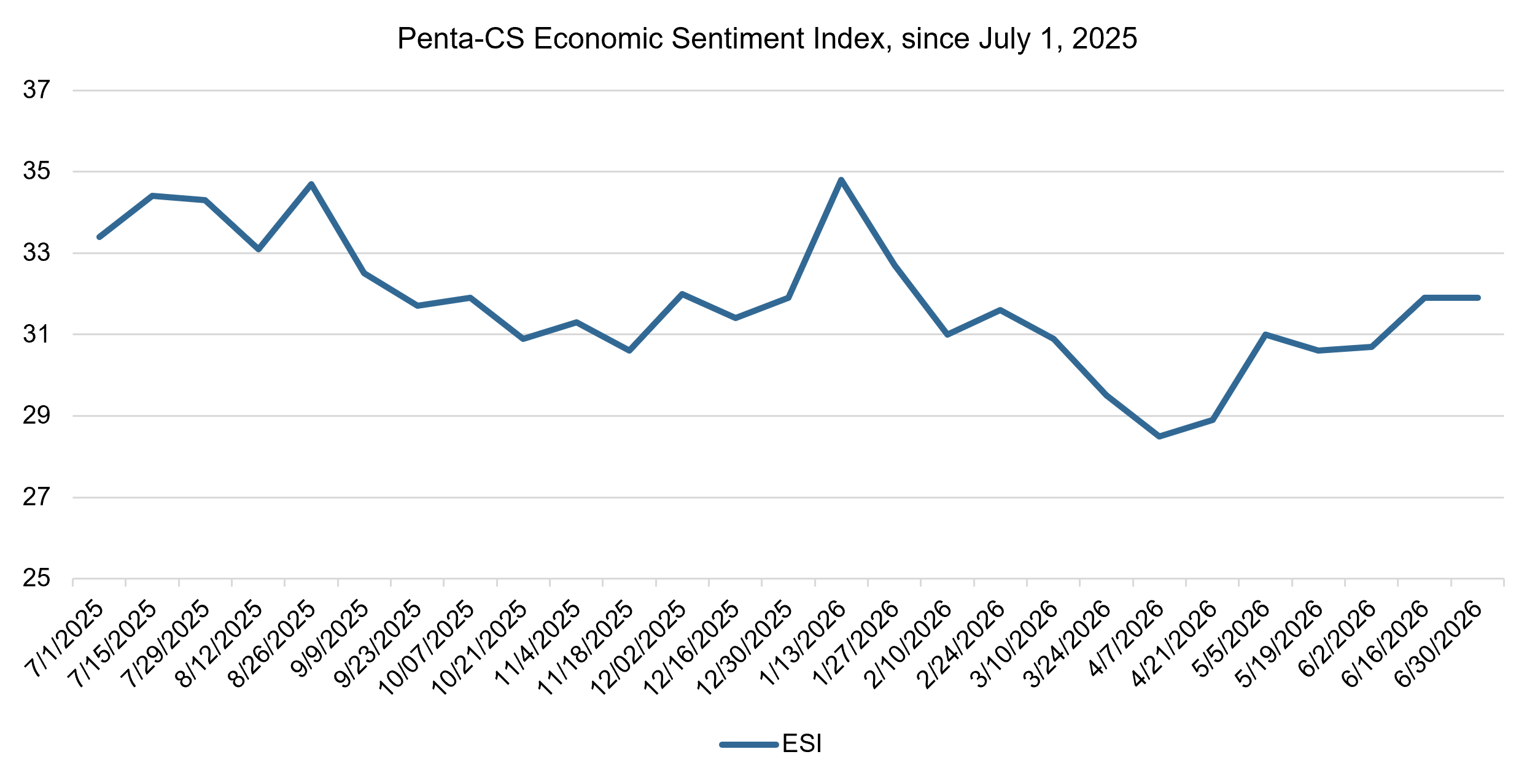

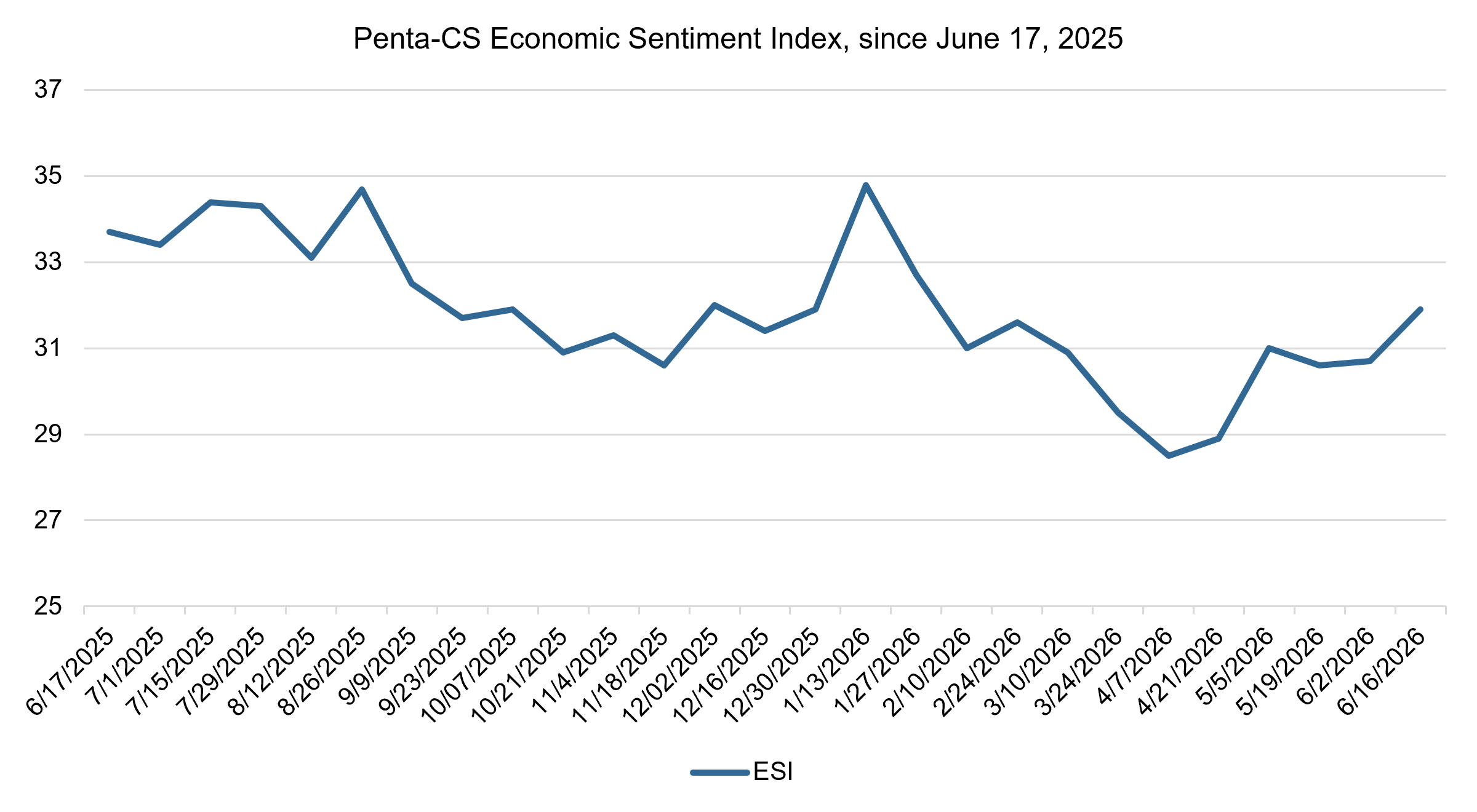

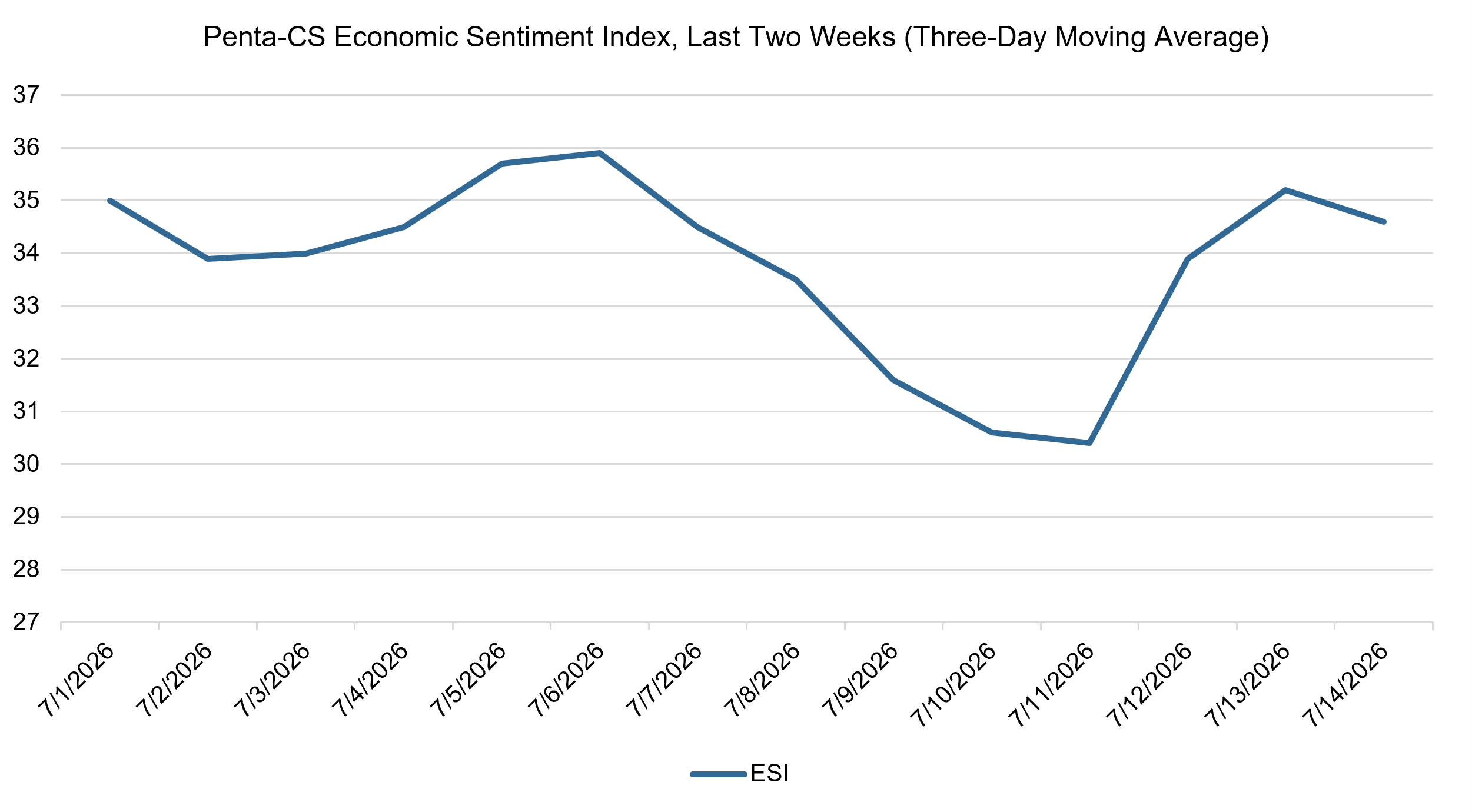

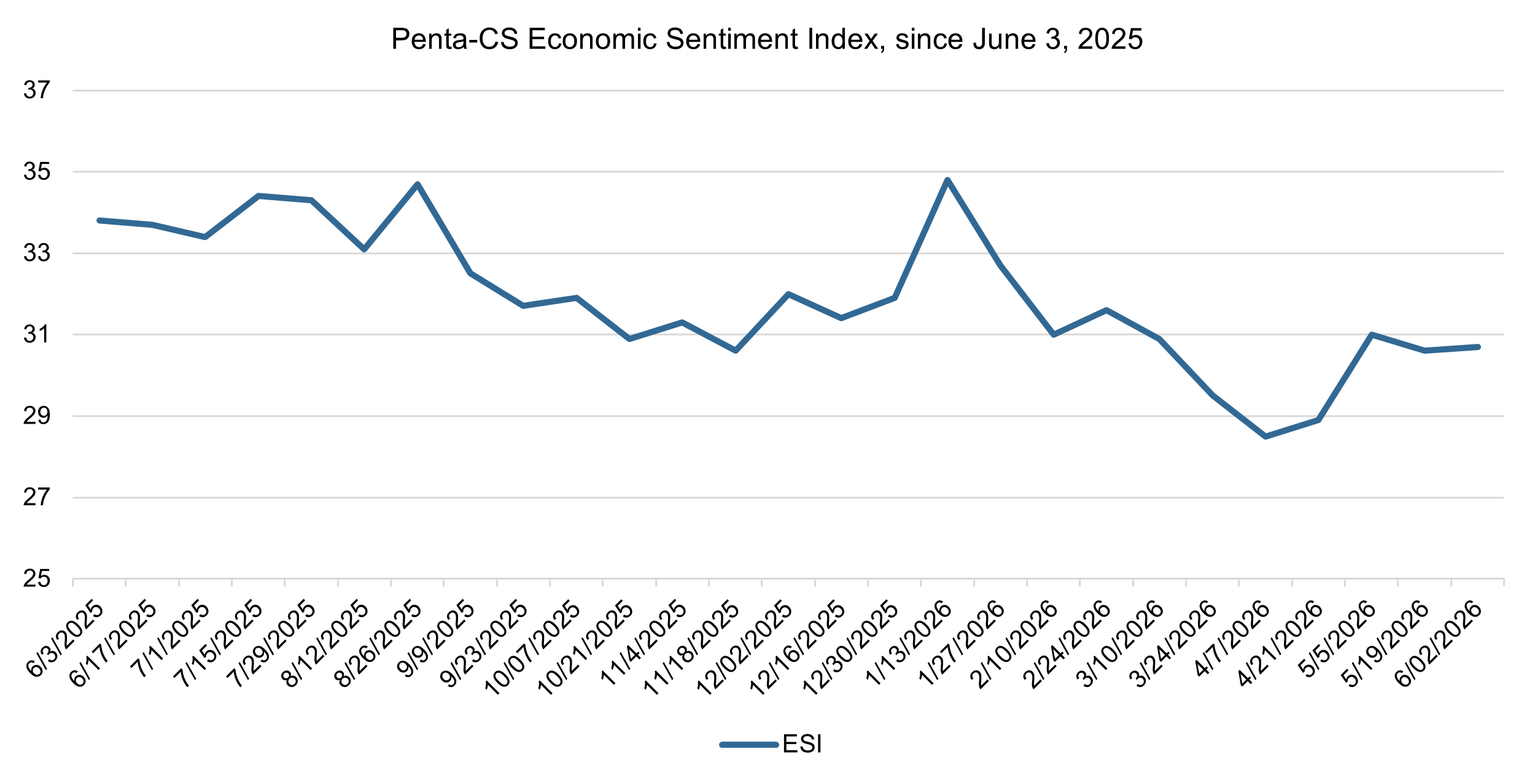

The latest biweekly reading of the Penta-CivicScience Economic Sentiment Index (ESI) decreased 2.6 points to 30.8 ahead of the July FOMC meeting, driven by renewed volatility as geopolitical conflict increased energy prices and the White House announced new tariffs.

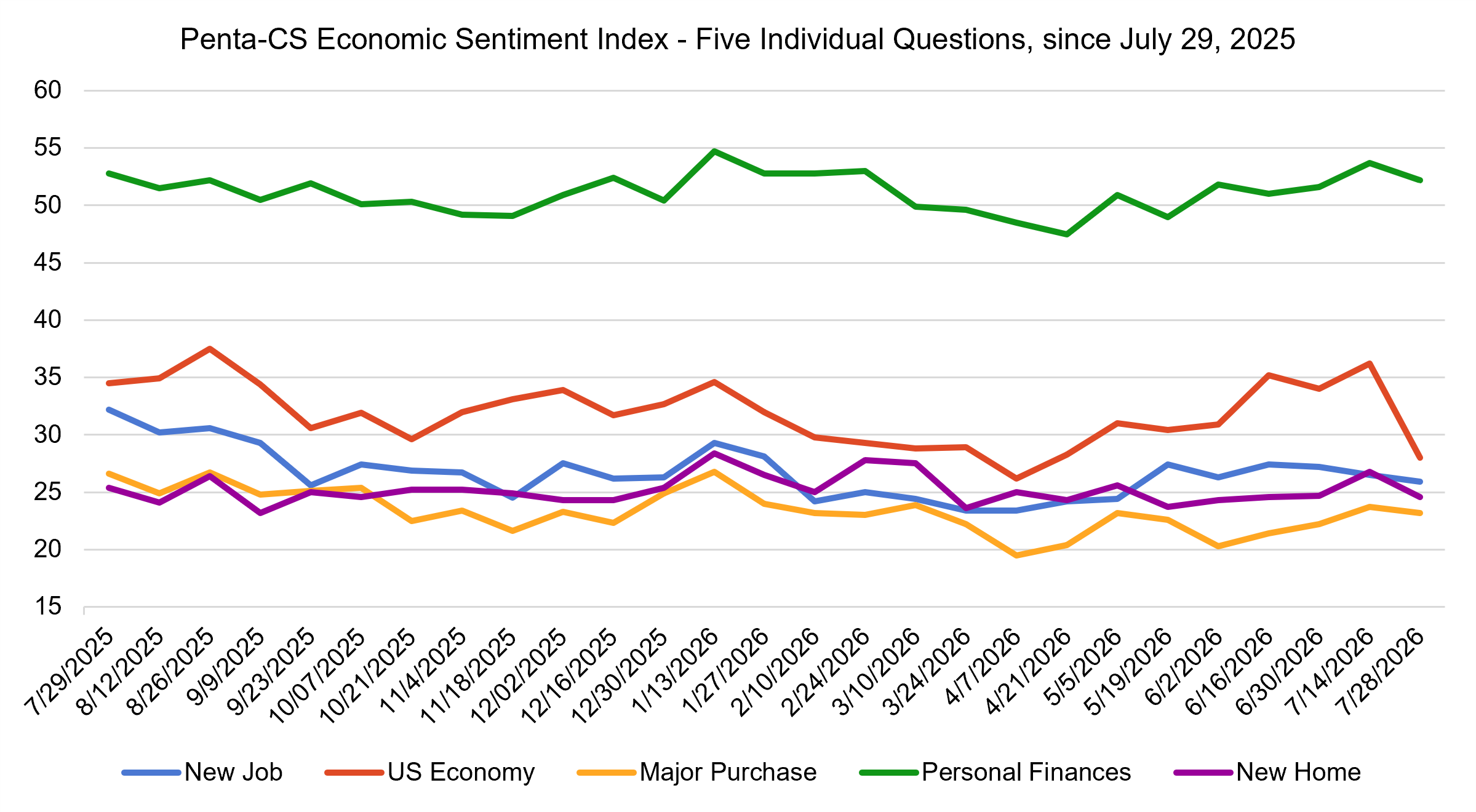

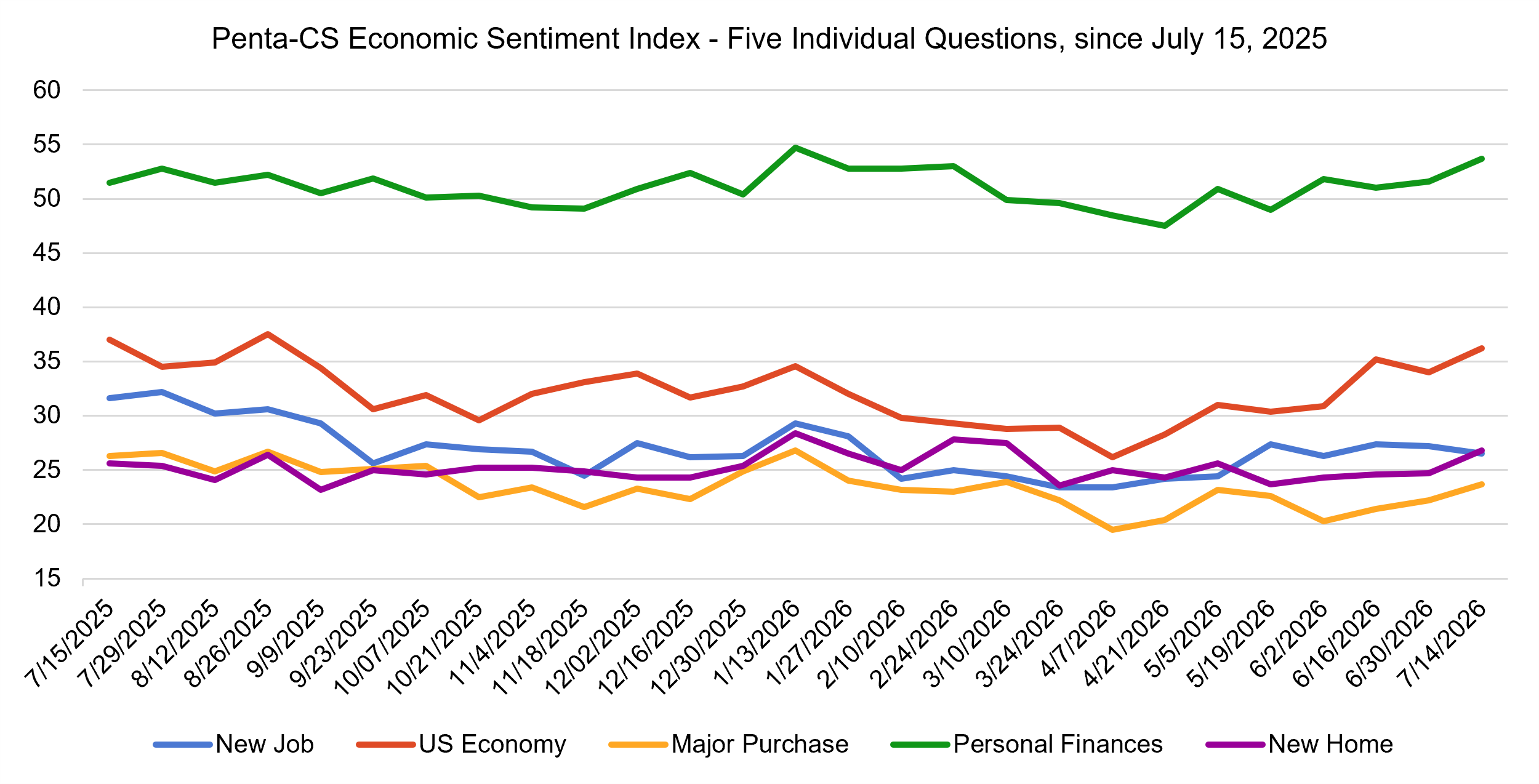

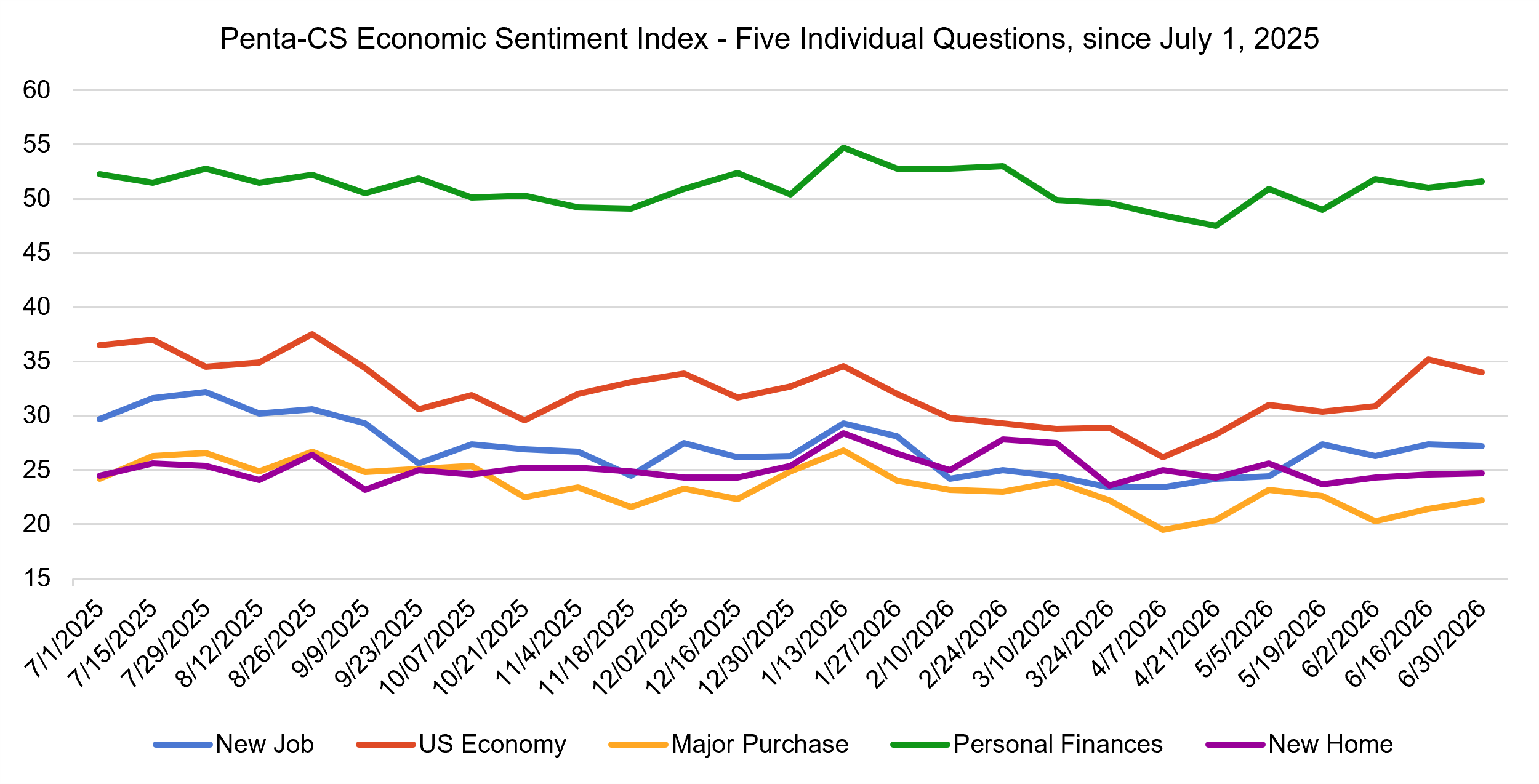

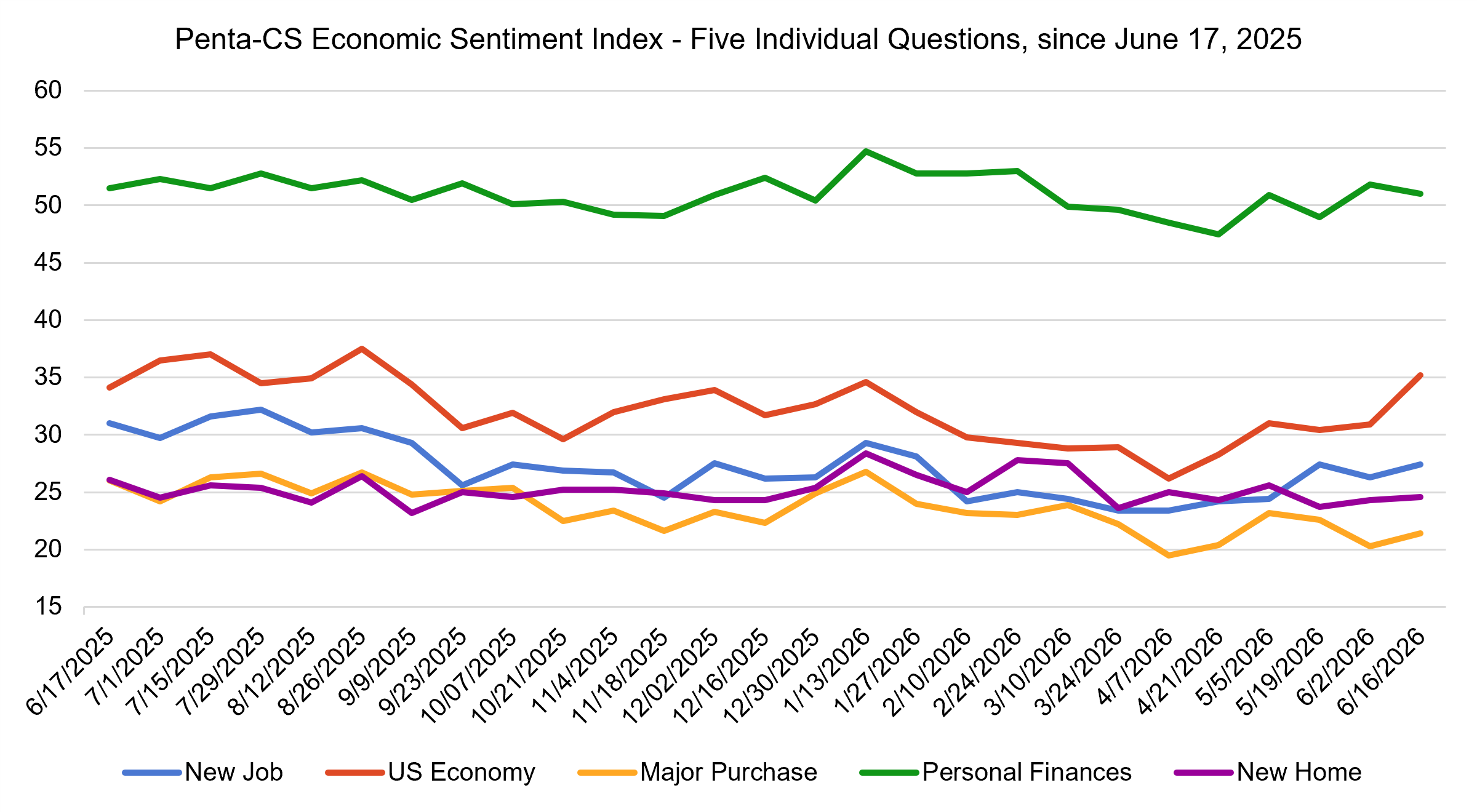

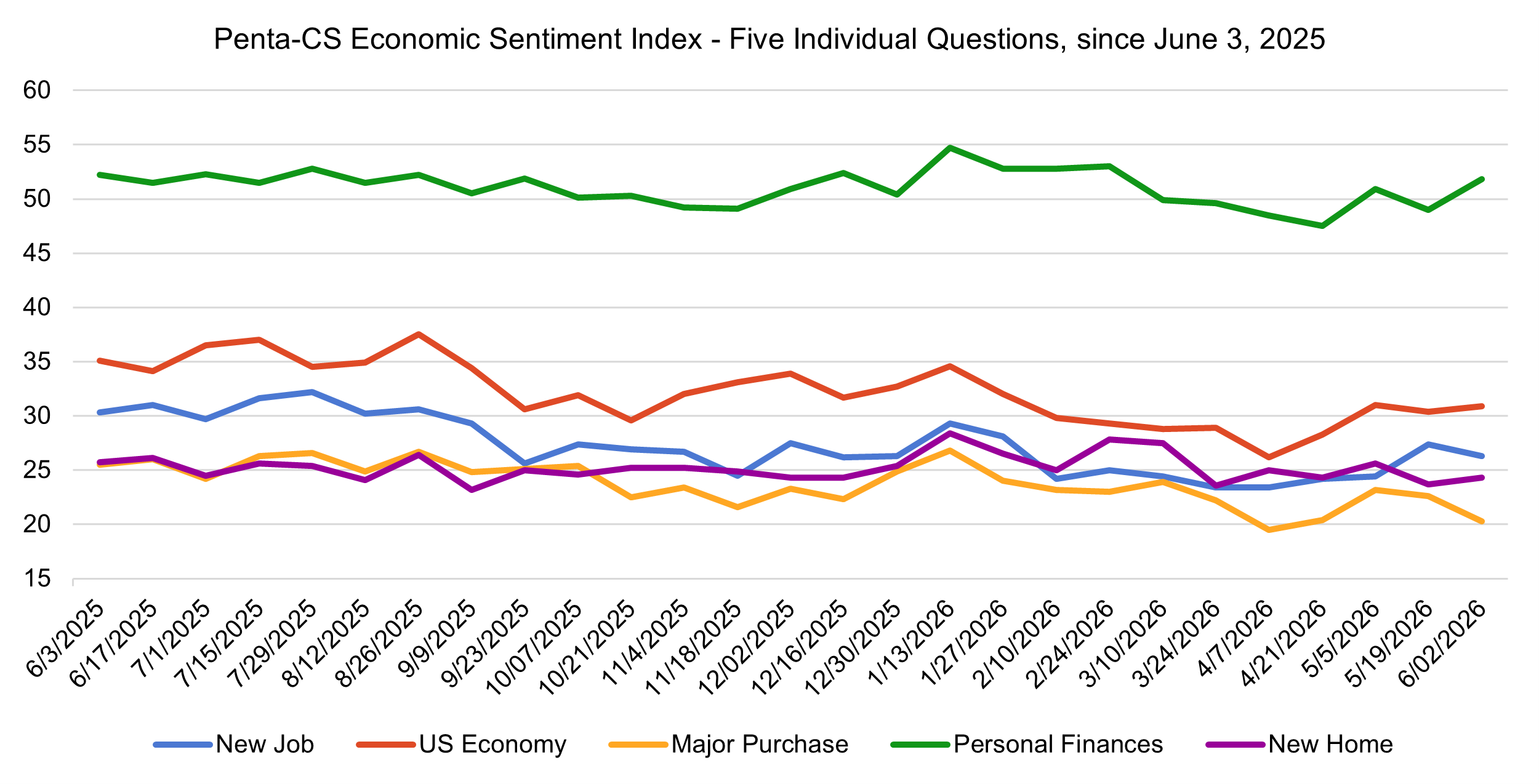

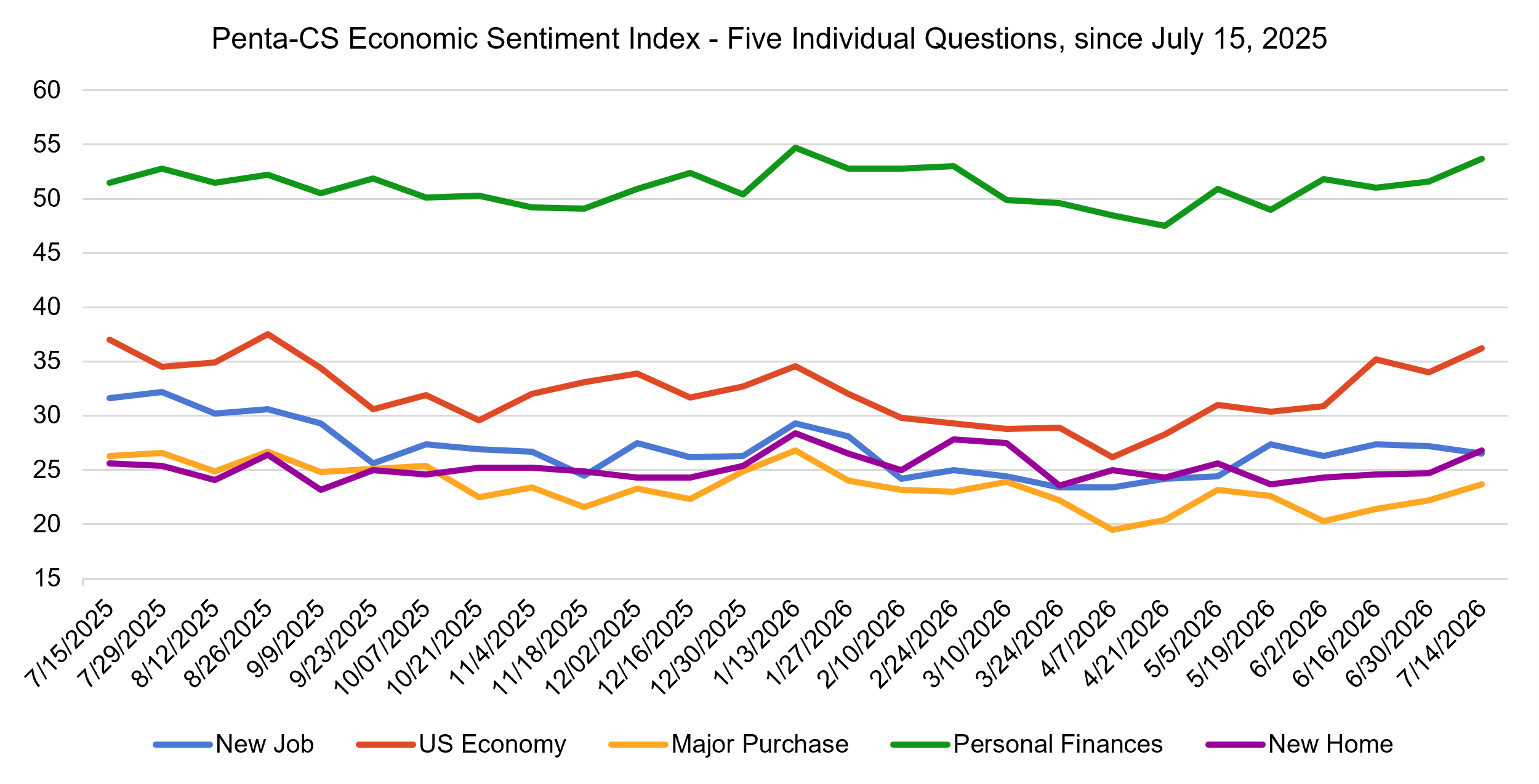

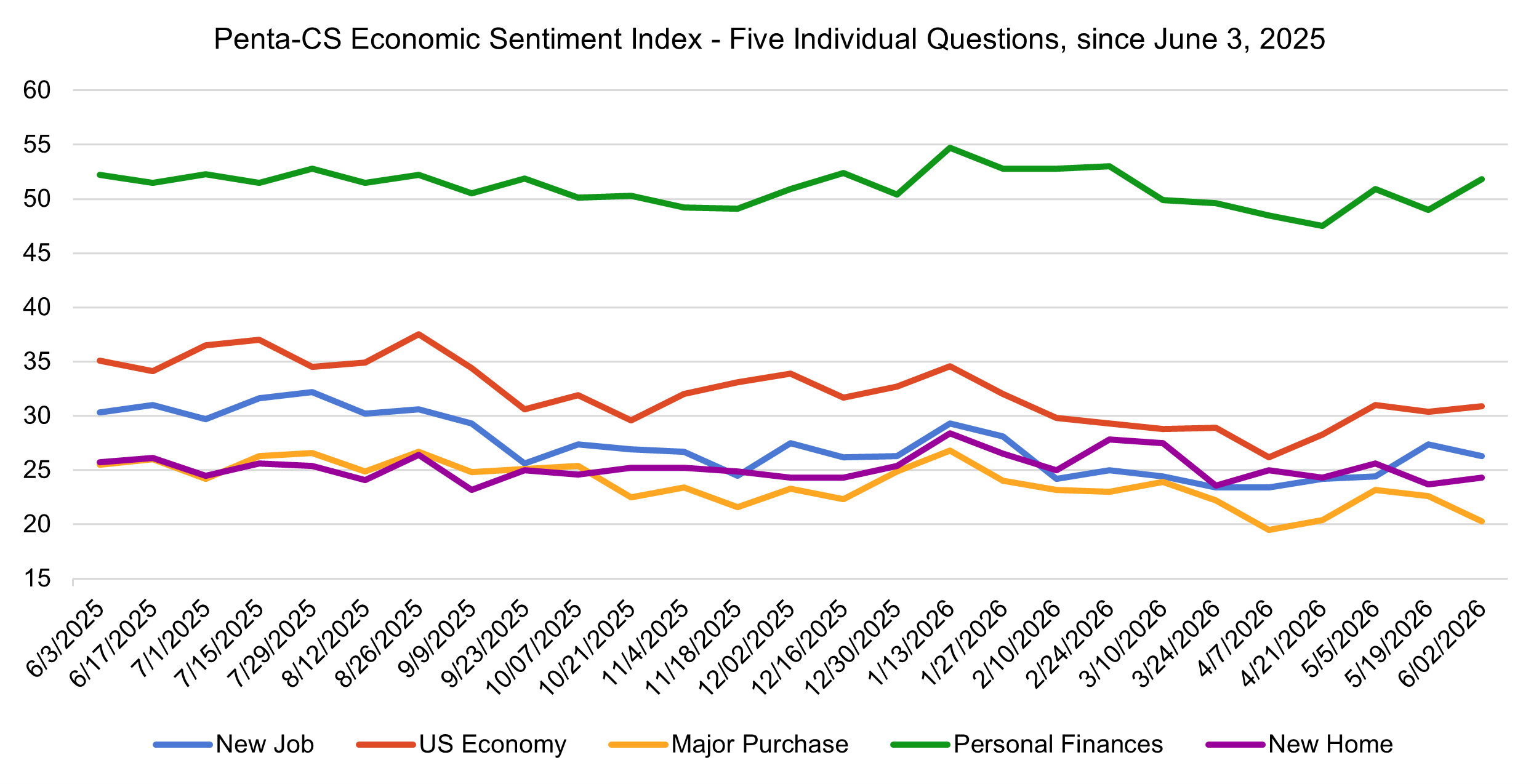

All five of the ESI’s indicators decreased during this period. Confidence in the overall U.S. economy decreased the most, falling 8.2 points to 28.0.

—Confidence in buying a new home decreased 2.2 points to 24.6.

—Confidence in personal finances decreased 1.5 points to 52.2.

—Confidence in finding a new job decreased 0.6 points to 25.9.

—Confidence in making a major purchase decreased 0.5 points to 23.2.

Renewed tensions between the United States and Iran pushed oil prices sharply higher as attacks on commercial vessels and military sites raised concerns about shipping through the Strait of Hormuz. Brent crude briefly rose above $100 per barrel before falling after the two countries paused attacks and diplomatic negotiations resumed. The renewed volatility in energy markets threatens to place additional pressure on gasoline prices and broader inflation, complicating the Federal Reserve’s interest rate decisions and adding another source of strain for consumers.

The Census Bureau reported that U.S. retail and food services sales increased 0.2 percent in June, following an upwardly revised 1.0 percent increase in May. Sales were 6.7 percent higher than a year earlier, signaling that consumer spending remained resilient despite elevated prices and borrowing costs. However, because the estimates are not adjusted for inflation and the monthly increase was modest, the report suggests that spending continued to grow without a significant acceleration in underlying consumer demand.

Housing starts increased 19.0 percent in June, driven primarily by multifamily construction, while single-family starts were largely unchanged and building permits fell 3.0 percent. New-home sales increased 1.6 percent but remained 5.6 percent below their level a year earlier, while the average 30-year fixed mortgage rate rose to 6.58 percent, the highest level in nearly a year. Together, the data suggest that high borrowing costs continue to weigh on prospective homebuyers despite some improvement in construction and sales activity.

On July 23, the White House announced new tariffs of 10 or 12.5 percent on imports from 60 trading partners that it determined had failed to impose or effectively enforce bans on goods produced with forced labor. The action applies to trading partners accounting for 99.4 percent of U.S. imports, although certain products and materials are exempted. These tariffs are effectively replacing a temporary 10 percent global tariff that was imposed following the Supreme Court’s decision to strike down the president’s “Liberation Day” emergency tariffs imposed under the International Emergency Economic Powers Act. The new duties could raise costs for businesses that depend on imported goods and add to inflationary pressure if companies pass those costs on to consumers.

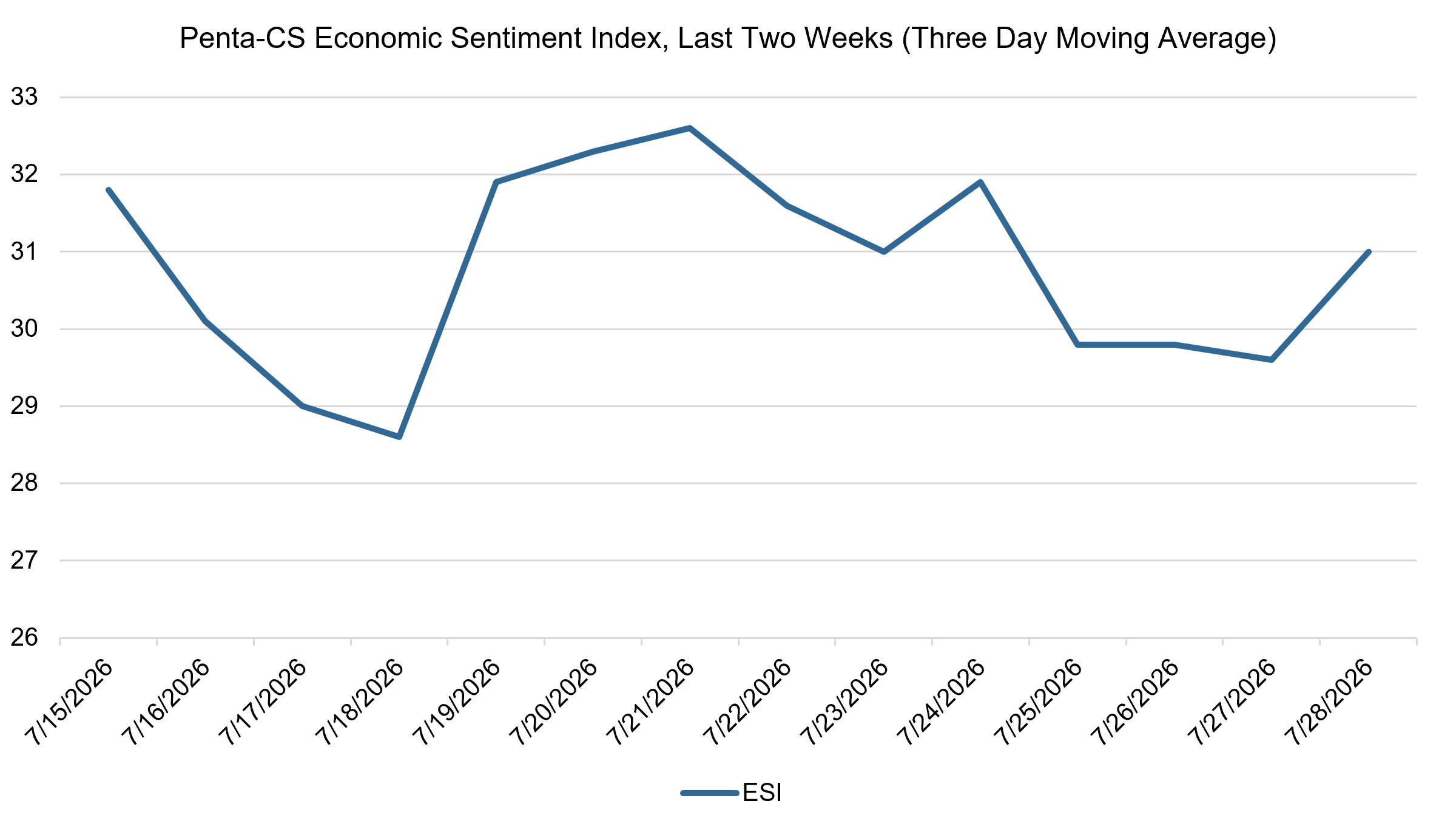

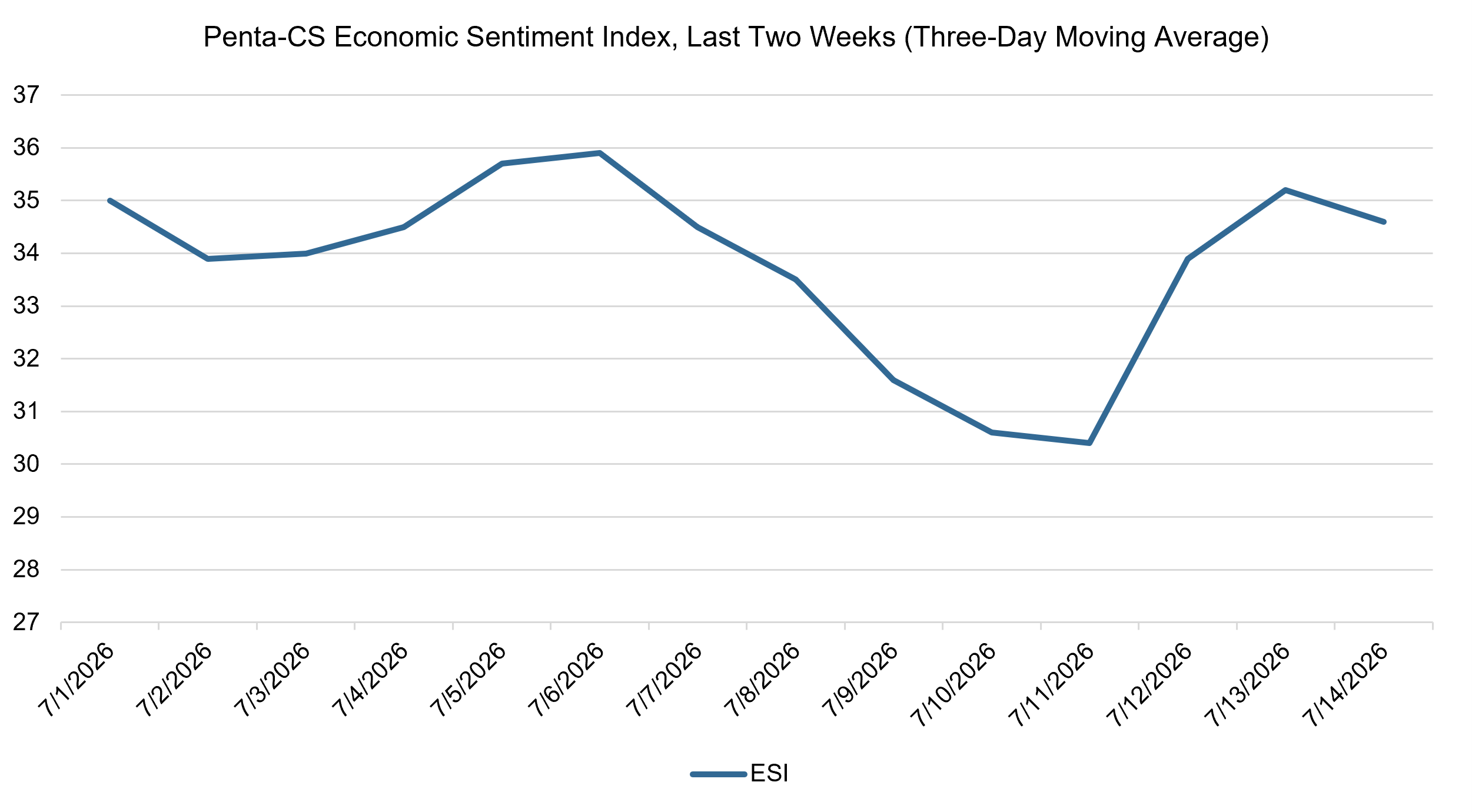

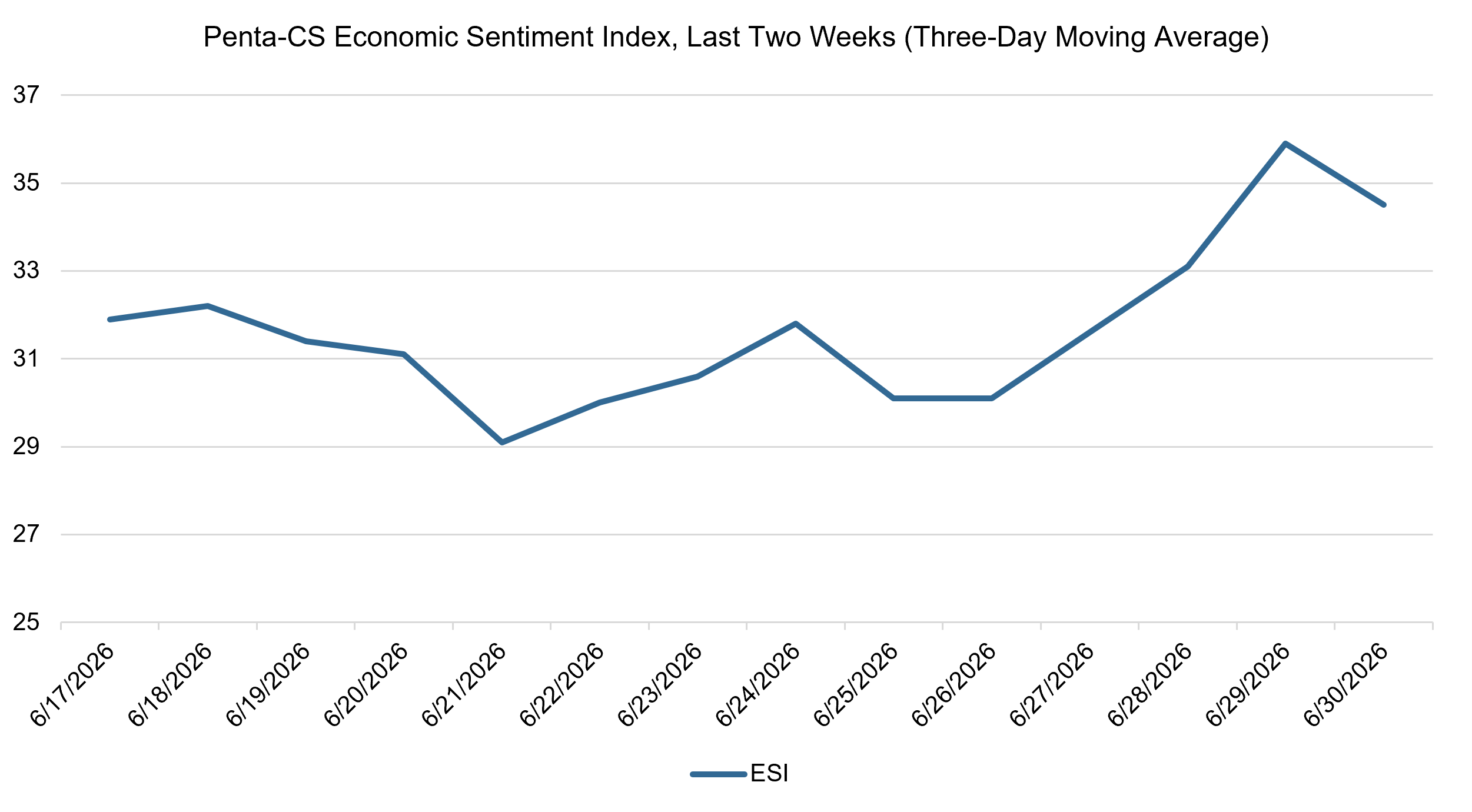

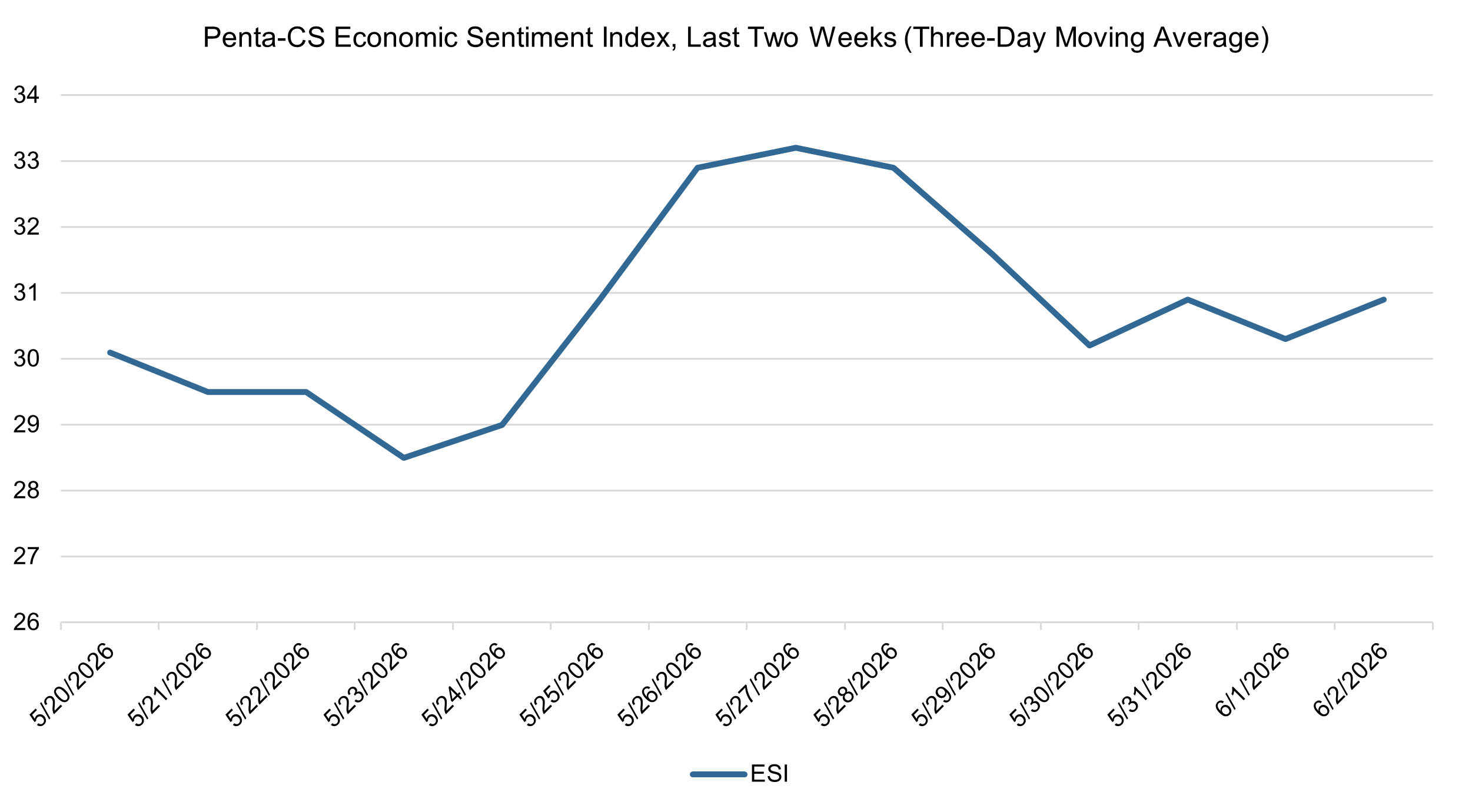

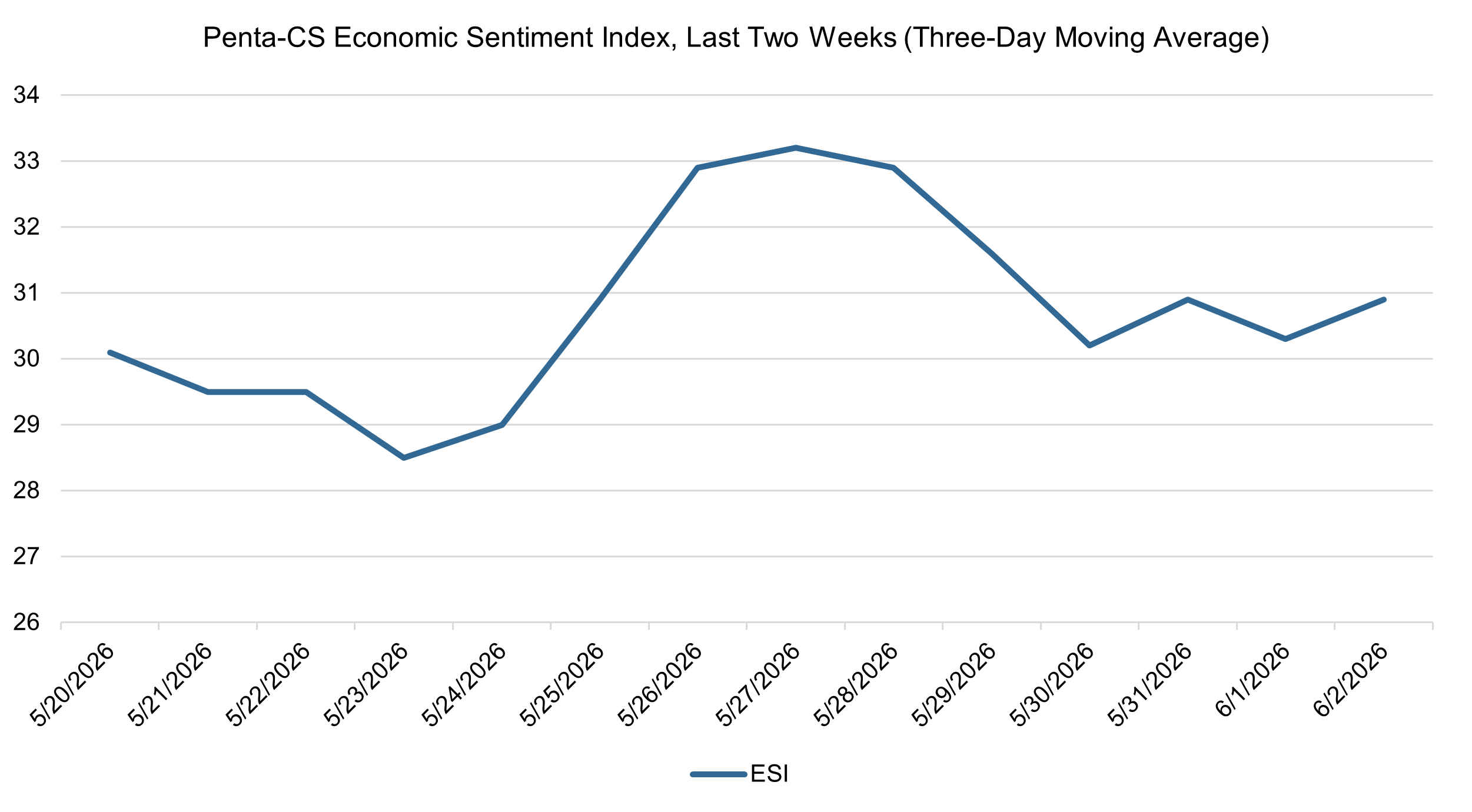

The ESI’s three-day moving average remained relatively stable over the two-week period, falling to a low of 28.6 on July 18 before climbing to a period high of 32.6 on July 21. The three-day moving average then oscillated before falling to 29.6 on July 27 and bouncing back to 31.0 to close out the session.

The next release of the ESI will be on Wednesday, August 12, 2026.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}